A week ago, hardly anyone was talking about a pre-election interest rate hike.

Now there is a tsunami of professional opinion pointing to an increase in the official target cash rate on Tuesday, following last week’s dramatic rise in inflation.

Prices are now rising at their fastest in 20 years.

For a government campaigning for re-election due to cost-of-living pressures, the March quarter figures delivered a hammer blow. Maybe not deadly, but extremely damaging nonetheless.

An official hike would only add to the pain and increase the political embarrassment.

But there is one thing the forecasters have overlooked. It has nothing to do with the independence of the Reserve Bank of Australia and its willingness to withdraw from the political process.

It’s this: the RBA really doesn’t want to raise interest rates – at least not to levels close to the levels that many now see as inevitable.

Certainly, there is a logical argument that with unemployment below 4% and headline inflation above 5%, the economy appears to be overheating. In these circumstances, there is no justification for emergency rates at 0.1%.

But over the past 30 years, the RBA – in association with banking regulator, the Australian Prudential Regulatory Authority – has helped create one of the biggest asset price bubbles in the world. And if it collapsed, it would wreak havoc on the financial system and the economy.

Australia is finally captive to real estate. We are not the only country to have allowed this to happen. But we are one of the most glaring examples.

Our banking system, which for decades thrived on skyrocketing house prices, has become hostage to a $9 trillion monster. And while our politicians for years berated themselves over relatively insignificant levels of public debt, they conveniently ignored Australia’s real economic Achilles’ heel: household debt.

It’s now hampered our central bank. He can’t raise the rates to anywhere near the required level without causing total chaos.

As perverse as it sounds, our perilous situation of personal debt could be the saving grace for those who have lately braced themselves for eyeballs.

We just can’t afford to have that many!

Rocks and hard places

Money markets are in collapse mode. Bond investors – here and around the world – suffered huge losses as a decades-long boom suddenly reversed as inflation awoke from a 30-year slumber.

Markets ultimately determine how much we pay to borrow money. And if you believe them right now, official rates should hit 3.5% by October next year.

This is the equivalent of 14 rate hikes in 16 months. Given our booming labor market and accelerating inflation, there is some logic to their argument, but it ignores a critical piece of the economic puzzle.

Rate hikes of this magnitude would send large numbers of Australians – mostly young, recent first-time home buyers – to the wall. This would severely depress the housing market, in turn putting the banking system under enormous pressure and plunging the economy into recession.

It just won’t happen.

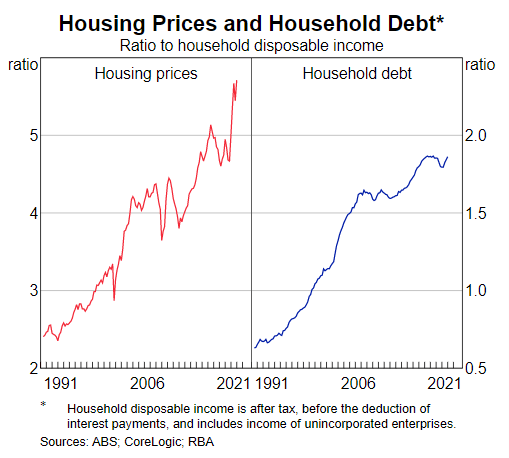

Here is a chart that the RBA released a few weeks ago. The left side shows how rich we all have become as real estate has skyrocketed relative to our income. On the right is the compromise. Australian households are carrying record levels of debt, secured by these expensive homes.

It really is a house of cards.

If you think that’s worrying, keep this in mind: the debt numbers are averages.

While it shows household debt at an all-time high at nearly double household income, large numbers of young Australians were allowed last year to borrow up to 6 times their income. About half a trillion dollars have been advanced during the pandemic.

If you need to know more, check out the extraordinary lending spree our banks have been on during the pandemic, all under the watchful eye of our regulators.

This dramatic increase in homeownership is largely coming from first-time homebuyers – most of whom thought there wouldn’t be an official rate hike for at least four years.

The banks thought so too.

safe as houses

In 2017, when real estate seemed to be heading for the moon and beyond, the RBA and the banking regulator caused a downturn in national property markets. They just made it harder to get a loan.

You can see the impact in the two charts above. Banks advanced less money, especially to investors, and prices began to moderate.

For a time, it appeared that we might have been able to achieve what many thought was impossible: remove the heat from real estate without serious economic side effects.

The pandemic has changed all that. With forecasts of a 20% property slump by even relatively sober analysts – as the economy plunged into the worst recession in a century – the RBA opened the floodgates. A dramatic drop in interest rates, coupled with lower prices, has presented a rare opportunity for first-time home buyers to dive.

The final result ? All that easy money fueled additional demand that first stabilized property markets before setting off into a frenzy. Rather than steep price drops, house prices have reached their highest levels in history.

It was a deliberate strategy. Since real estate is our household’s main asset, higher prices make homeowners feel wealthier, which encourages them to spend more. This helps stimulate economic growth. This is called the “wealth effect”.

But it also works in reverse. Falling prices are making everyone nervous. They spend less, which can snowball into a recession. And since mortgages make up about 60% of our bank’s loans, a real estate crash can cause a financial crisis.

It was the spark that ignited the incendiary known as the global financial crisis. This is why the RBA acted the way it did in 2020. And why it will be much more cautious in rate hikes than the horror predictions you hear right now.

He’s in no mood to crush the economy and sink our banks.

Rates and recession

If the prospect of a potential slowdown in the economy isn’t enough to send shivers down the spine of our central bank’s Martin Place headquarters, the world’s increasingly nervous warnings of an impending recession will.

US inflation is accelerating at its fastest pace in 40 years. That’s what you get when you print $5 trillion ($7 trillion) in new money and the government pumps out billions more in new spending.

The economy recovered faster than expected, factories took longer to get back up and running than expected, and transportation and logistics struggled to keep up. To this heady mix of huge demand and supply shortages, add a war in Europe that has disrupted energy, food and metals.

The end result is runaway inflation. And the solution, which has been slow to take off, increasingly seems to be a series of sudden and very large interest rate hikes. The US Federal Reserve is expected to double hike later this week.

To calm inflation, it will try to slow down domestic demand and growth.

But here’s the thing: cutting off growth without snuffing it out completely is an incredibly difficult balancing act. If that weren’t complicated enough, China’s increasingly fruitless war against the Omicron variant has resulted in hundreds of millions of citizens being locked out, raising serious questions about its economic prospects and impact on the rest of the world. .

There is a conga of investment banks trying to predict the depth of the coming recession. Most of them cite the risk that central banks put the brakes on too hard and too late.

Meanwhile, the International Monetary Fund and the World Bank significantly lowered their growth forecasts last week.

What are the chances of 14 successive rate hikes in this environment?

Of them. Buckley and none.

So, no need to panic just yet.

Loading the form…